New customer onboarding in banks is not a simple handoff, particularly for commercial bankers. By the time a new client relationship is live and transacting, your team has coordinated the onboarding process across relationship management, operations, compliance, legal, and sometimes treasury, often over weeks (or months) and often over email.

It’s incredibly important that banks ensure this process is as efficient as possible, particularly given the amount of trust required to maintain a relationship with their clients and in how they realize revenue (often during setup and when financial products are activated). In other words, onboarding has to be efficient and build trust for banks to continuously grow revenue through commercial banking.

We’re hearing from more and more teams recently that recognize that this aspect of their client lifecycle is underinvested and insufficient. They’re turning to purpose-built customer onboarding software to help.

Let’s break down why customer onboarding is so influential for banking relationships and how banks are using customer onboarding software today.

Where Onboarding in Commercial Banking Breaks Down

Customer onboarding in banking gets complicated fast, and the compliance steps get most of the attention. Rightfully so. Customer onboarding KYC and KYB documentation for a commercial client means collecting entity formation documents, tax IDs, and ownership structures that often go three or four layers deep. Beneficial ownership requirements add another layer—identifying and verifying every individual with 25% or more control, navigating holding company structures, and chasing documentation from people who didn’t know they’d be part of the process.

None of that is optional. And in order to be efficient, it’s deeply reliant on each internal and external stakeholder participating in the process.

To ensure each stakeholder is accountable for completing what is needed from them to move onboarding forward, you need two things:

- Transparency—they should know exactly what’s required from them, by when, and how their participation moves the process forward.

- Engagement—they’re busy and probably distracted. They need relevant, visible reminders that get them to take action.

These two things matter for practical reasons. A client who knows what’s coming and why moves faster than one who’s fielding requests that feel random or redundant. When relationship managers, compliance teams, and operations are working from the same information, they move faster.

The Multi-product Layer Makes it Even More Complicated

A typical commercial banking client doesn’t purchase one product. Generally, banks are required to onboard clients to operating accounts, ACH origination, wire services, a treasury management platform, and sometimes a commercial card program. Each has its own configuration requirements, approval chain, and documentation threshold.

The sequencing matters, and the dependencies are real. You can’t provision ACH origination until the account is open. You can’t configure the treasury portal until the account is provisioned. You can’t train the client’s AP team until the portal is live. Every dependency is a potential friction point, and when those handoffs happen without clear structure, transparency, and reminders, they can cascade into a failure to launch.

What Good Customer Onboarding in Banking Requires Operationally

Improving your onboarding operations requires being honest about what your current stack can and can’t do.

Email can communicate, but it struggles to coordinate. A shared tracker on Excel shows status but doesn’t really drive accountability. A CRM tells your RM where a deal stands but doesn’t tell your client’s controller what they still owe you. The tools most commercial teams use to manage onboarding were built for something else, and the workarounds are consuming real capacity.

That’s the pattern we built GUIDEcx to break and why purpose-built customer onboarding software for banks solves something that general project management tools simply weren’t designed to handle.

Customer onboarding software like GUIDEcx doesn’t fully remove the coordination costs involved in commercial banking onboarding. The KYC and KYB requirements remain. The documentation requirements remain. The internal handoffs between relationship management, operations, compliance, and treasury teams still have to happen.

But it does change how the work is coordinated. For banks, that looks like this:

Instead of managing onboarding across email threads, spreadsheets, and disconnected internal systems, customer onboarding software creates a structured environment around the onboarding itself. Every participant in the process — internal teams and the client — can see what has been completed, what is required next, and who is responsible for moving it forward.

This structure tends to solve several of the operational issues that slow onboarding in banking today.

First, it creates visibility across stakeholders. Relationship managers, operations teams, compliance staff, and the clients can all reference the information they need to perform their tasks and confidently understand the status of their progress.

Second, it creates clear accountability for tasks and documentation. Instead of requests being distributed across emails or individual follow-ups, required steps are tied directly to specific owners with defined due dates.

Third, it introduces consistency across onboarding engagements. When each new commercial client follows a structured onboarding framework, teams avoid reinventing the process for every relationship or product configuration.

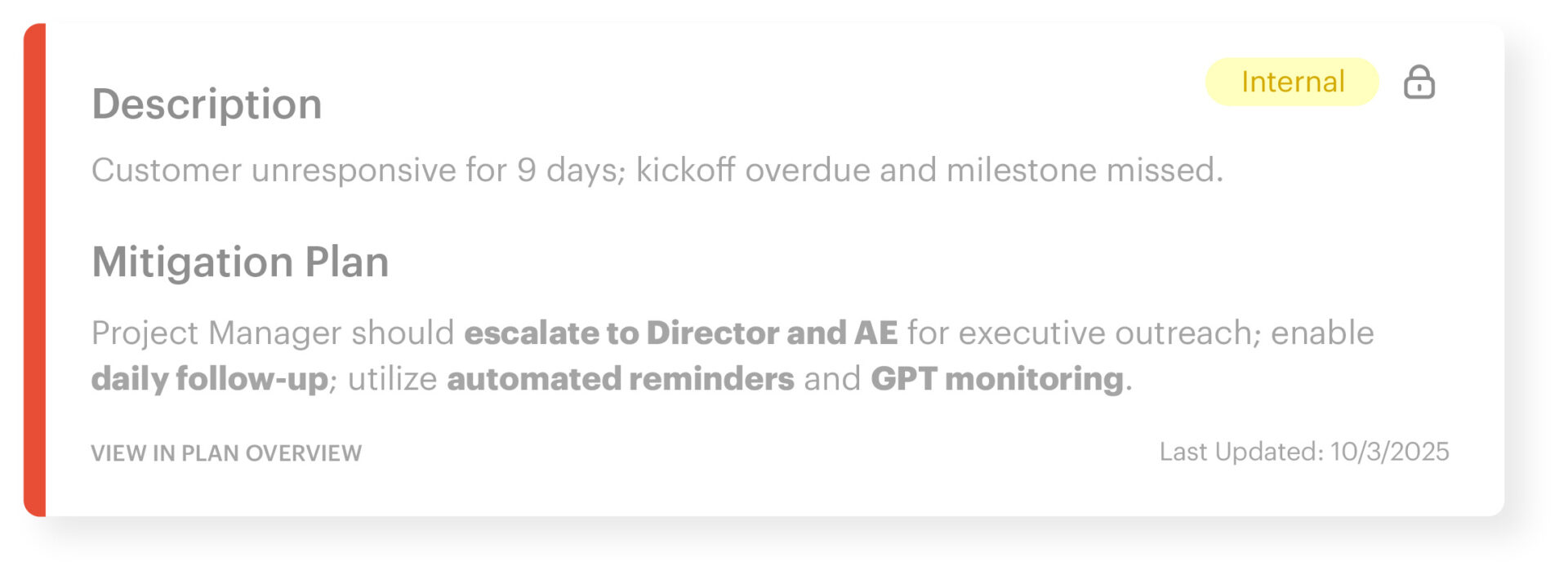

Finally, it provides operational insight into onboarding performance. Leadership can see where projects are progressing smoothly and where dependencies or delays are emerging, often early enough to intervene before the experience degrades for the client. GUIDEcx does this with RAG Agentic Coach, an AI Agent that proactively spots risks and suggests mitigation plans for your team to fix them.

RAG Agentic Coach in GUIDEcx—an AI Agent that spots risks in onboarding projects

In practice, the goal of onboarding software in banking should be to bring structure, transparency, and accountability to a process that has historically been coordinated through tools that were never designed for it.

And as more banks begin to focus on the onboarding phase of the client lifecycle, the teams that treat onboarding as an operational system are the ones that tend to move faster, activate clients sooner, and build stronger commercial relationships over time.

- Customer Onboarding is One of the Most Complicated Challenges in B2B – May 27, 2026

- Introducing Dana Okerlund, Director of Product at GUIDEcx – May 21, 2026

- Introducing Chris Griffith, Chief Technology Officer at GUIDEcx – May 19, 2026